The global display market is facing continued pressure, with Omdia forecasting a further decline in professional display demand for 2025. While these figures only partially reflect the digital signage sector, manufacturers confirm a slowdown – driven by tariffs, shifting technologies, and changing market dynamics.

")

Omdia Forecasts Decline: What It Means for Digital Signage

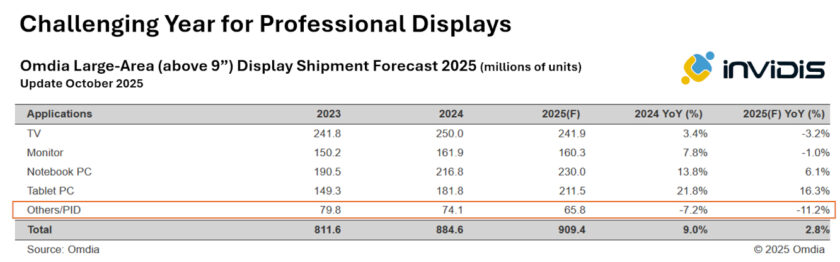

The global market for professional displays continues to face headwinds. According to the latest October update from Omdia, global demand for professional displays is expected to decline by -11.2% in 2025, following a -7.2% drop in 2024. While the overall display market shows modest resilience with projected growth of +2.8%, the professional segment remains under pressure.

However, these figures only partially reflect the reality of the digital signage and ProAV industries. Omdia’s data includes Professional Information Displays (PIDs) starting from 9 inches, encompassing a wide range of use cases such as hotel TVs and small-format displays that are not relevant for most digital signage applications. Only displays 32 inches and larger are typically used in signage environments.

Market feedback confirms mixed picture

Despite the limited relevance of the Omdia data for the signage industry, display manufacturers have confirmed to invidis that demand for professional displays in the digital signage segment remains muted. In particular, punitive tariffs in the U.S. have led to a double-digit decline in shipments to the U.S. during Q2, further dampening market momentum.

The declining shipment figures also reflect a broader technology shift. While LCD and OLED volumes are down, LED-based solutions are gaining ground – not yet in unit shipments, but increasingly in revenue share. This trend is reshaping the display landscape, especially in high-end and large-format installations.

Growth is slowing down

In Europe as in the rest of the world, the digital signage market has largely recovered from the pandemic, but the era of double-digit annual growth appears to be over. For 2025, growth is expected to remain in the low single-digit range. However, with Q4 traditionally being the strongest quarter, the final weeks of the year will be decisive in determining the industry’s overall performance.